Capital Asset Pricing Model (CAPM)

Before going into details of the Three Factor Model, it's first important to have a brief understanding of the Capital Asset Pricing Model (CAPM) on which the Three Factor is largely based. CAPM basically only uses market risk (systemic and non-systemic) as a proxy for expected return. Its equation is Ra = Rf + Ba(Rm - Rf), where Rf is the risk free rate of return, Ba is the beta of the security, and Rm is the expected market return. Essentially, as explained by this equation, investors are compensated by risk as measured by beta and time value. As investopedia explains:

Eugene Fama, a professor at Booth, and Kenneth French , a professor at Tuck, developed a model by which to further describe market behavior, expanding on the CAPM. They published their findings in the Journal of Finance in 1992 ("The Cross-Section of Expected Stock Returns") and provided more details a year later in the Journal of Financial Economics ("Common Risk Factors in the Returns on Stocks and Bonds"). While CAPM uses the single factor of beta to compare returns, Fama and French found that to be too simplistic of an approach and added both size and value as factors to the model. They found that historically stocks with high book-to-market ratios (i.e. value stocks) and small-cap stocks have performed better than the market at large. Thus, they simply added to the end of the CAPM equation expressions SMB ("small (market capitalization) minus big"), HML ("high (book-to-price ratio) minus low"), and alpha. This new equation accounts for the tendency of outperformance of these two factors and gives a better comparison tool for evaluating fund performance, among other uses.

The important part of their findings to us as individual investors and the main take home message is value stocks tend to perform better than growth stocks and small caps typically outperform large cap companies. Thus, portfolios with a high percentage of small cap and value would result in a lower value using this model than the CAPM, since it adjusts downward on those two accords.

Here is another chart from Index Funds Advisors, showing the growth of $1 from 1928 to 2007. The annualized return is on the y-axis while risk in the form of standard deviation is on the x-axis. Small-value experienced a 14.6% annualized return (albeit with higher risk) while large-growth had a 9.6% annualized return through December 2004. One interesting datapoint on this chart is small-growth, which has historically had relatively weak returns with a high standard deviation.

Small-Value Premium

Not only do small-cap and value plays have higher expected return, but they also provide additional diversification. While one may think that simply "owning the entire market" is as diversified as one can get in US equities, the weighting mechanism that indices use is "a far different outcome from what one would expect," explains Larry Swedrow in What Wall Street Doesn't Want You to Know. "Almost 70% of the portfolio is large-cap growth stocks." He recommends putting a large percentage of the portfolio in small-cap or value funds to compensate for this perhaps seemingly bizarre weighting. When your large-cap growth zigs, your small-cap or value holdings may zag, enabling you to sustain performance even in bearish times. Of course, these asset classes aren't perfectly negatively correlated so it's not going to be a flawless zig/zag relationship (nothing is unless you're shorting and long in the same position, which would be pretty pointless), but at least it presumably provides protection against the downside while at the same time increasing your expected return. A double win!

As stated above with the Fama French Model, but it doesn't hurt to emphasize this point, since small-caps and value typically carry larger risks, the expected return must be greater to compensate. This is the small-value premium that people seek.

What this means for your portfolio

Personally, I think it makes the most sense for individual investors to simply hold small-cap value and ignore small-blend and large value. I find this simplified approach meets the desired results and is easier to hold and maintain in a tax efficient manner. Some aggressive investors prefer a 50/50 split between total stock and small-value. I personally like approximately a 2:1 total stock to small value ratio. Value, small-cap, and small-cap value funds are typically less tax efficient than a total stock market fund counterpart, so it probably makes sense to hold the small-cap value in retirement accounts. Although examining the tax cost ratio via Morningstar of a fund like VISVX (Vanguard Small-Cap Value Index) shows the difference is negligible (in fact, VISVX seems to be more tax efficient than VTSMX over certain periods) , so holding it in taxable account certainly isn't the worst thing you could do.

Remember the media calling 2000-2010 the "lost decade" as the S&P was virtually unchanged? Well, if you had invested a considerable sum in small-cap value, your portfolio would be in seriously positive territory for that period. Not so lost anymore! From January 14, 2000 to June 10, 2010 (today), Vanguard Total Stock Market is down nearly 17%. It certainly would seem like a waste of investments if that was your return after 10 whole years. VISVX, on the other hand, is up 64% over the same period - an outperformance of 81%! And you thought those timing strategies had good outperformance. This strategy simply calls for setting a slightly different asset allocation and letting it be (which is much more tax efficient) and absolutely obliterated more complicated, tax-inefficient strategies.

Let's take a look at the growth of $10,000 chart of Total Stock Market and Small-Cap Value since June 1998. The blue line is total stock, while the orange line is small value.

As you can see, from 1998 to mid-2000, the total stock market largely outpeformed small-cap value as tech growth stocks were all the rage and escalated in value like no other time in history. When the tech bubble burst in 2000, though, you'd certainly be glad you had small-cap value to provide diversification and to offset some risk. In the 2000 to January 2003 period, the total stock market plummeted 36%, while small-cap value enjoyed a small (but real) 4% gain. That is the zig/zag action we were talking about earlier. The 1998-2003 timeframe illustrates this diversification benefit perfectly. While the total stock market took you on a roller coaster ride (where your $10,000 grew to $13,000 before falling to $8,000), small-cap value had a different trajectory and would have somewhat abated that volatility (for both the upside and downside).

In the end, after twelve years your $10,000 invested in VTSMX grew to nearly $12,000, while small-cap value blossomed to nearly $19,500. That's the small-cap premium we're looking for!

Just as a comparision, here is a chart comparing total stock (blue) with value (yellow), small blend (green), and small-value (orange). As you can see (although this won't always be the case), small-value really provides the best of both worlds in the Fama French model.

This strategy should be in the arsenal of all indexing individual investors. Small-cap value provides greater expected return and increased diversification with the caveat that one should expect slightly more volatility and risk.

Edit: DIY Investor brought up a good point in the comments that investors with lower risk tolerances (e.g. retirees) might want to think twice before "loading up" on these asset classes based on the downside risk, standard deviation, and volatility measures. I certainly agree and probably should have mentioned this above as there is certainly is increased risk in these asset classes. However, as I responded, I think investors are more than amply compensated for the additional risk. A retiree with a 40/60 equities/bonds portfolio might have something like 20% Total US, 10% Foreign, and 10% US Small Value based on my proposed 2:1 US Total to small value. 10% Small-Value, even with its volatility, is not going to wreak havoc on that portfolio and would marginally increase your risk (while correspondingly increasing your expected return). Looking at the alpha measures of VISVX (quite simply, a risk-adjusted measure of performance; of course, past performance doesn't guarantee future results), VISVX has a 3-year alpha of 6.68 (with a beta of 1.28) and a 1-year alpha of 6.68. That is, VISVX has enjoyed nearly a 7% outperformance (annually) of what CAPM would predict (i.e. after taking risk/beta/volatility into account). VTSMX, for comparison has an alpha of 1.18 (and beta of 1.03, as expected). As stated, this doesn't guarantee anything for the future, but historically the alpha values for small-value are favorable and investors have been more than compensated for the increased risk. But, it is important to stress, that the increased risk is real, so you should take this into account if you plan to dip in this asset class.

Update 6/16/10: Larry Swedroe's recent article on why the Small Growth Index is the "Black Hole of Investing." That's why I avoid it all together.

The CAPM says that the expected return of a security or a portfolio equals the rate on a risk-free security plus a risk premium. If this expected return does not meet or beat the required return, then the investment should not be undertaken. The security market line plots the results of the CAPM for all different risks (betas).Fama and French Three Factor Model

Eugene Fama, a professor at Booth, and Kenneth French , a professor at Tuck, developed a model by which to further describe market behavior, expanding on the CAPM. They published their findings in the Journal of Finance in 1992 ("The Cross-Section of Expected Stock Returns") and provided more details a year later in the Journal of Financial Economics ("Common Risk Factors in the Returns on Stocks and Bonds"). While CAPM uses the single factor of beta to compare returns, Fama and French found that to be too simplistic of an approach and added both size and value as factors to the model. They found that historically stocks with high book-to-market ratios (i.e. value stocks) and small-cap stocks have performed better than the market at large. Thus, they simply added to the end of the CAPM equation expressions SMB ("small (market capitalization) minus big"), HML ("high (book-to-price ratio) minus low"), and alpha. This new equation accounts for the tendency of outperformance of these two factors and gives a better comparison tool for evaluating fund performance, among other uses.

The important part of their findings to us as individual investors and the main take home message is value stocks tend to perform better than growth stocks and small caps typically outperform large cap companies. Thus, portfolios with a high percentage of small cap and value would result in a lower value using this model than the CAPM, since it adjusts downward on those two accords.

(click to enlarge)

As you can see from the above chart courtesy of the New York Times (who used Fama and French's data), since 1926 small-cap value companies have hugely outperformed large-cap growth firms. Note that this is on a logarithmic scale and not linear, so the outperformance doesn't look as dramatic as it could. But this is a nearly a 100-fold (or 10,000%) difference!Here is another chart from Index Funds Advisors, showing the growth of $1 from 1928 to 2007. The annualized return is on the y-axis while risk in the form of standard deviation is on the x-axis. Small-value experienced a 14.6% annualized return (albeit with higher risk) while large-growth had a 9.6% annualized return through December 2004. One interesting datapoint on this chart is small-growth, which has historically had relatively weak returns with a high standard deviation.

(click to enlarge)

Source: Index Funds Advisors

Source: Index Funds Advisors

Small-Value Premium

Not only do small-cap and value plays have higher expected return, but they also provide additional diversification. While one may think that simply "owning the entire market" is as diversified as one can get in US equities, the weighting mechanism that indices use is "a far different outcome from what one would expect," explains Larry Swedrow in What Wall Street Doesn't Want You to Know. "Almost 70% of the portfolio is large-cap growth stocks." He recommends putting a large percentage of the portfolio in small-cap or value funds to compensate for this perhaps seemingly bizarre weighting. When your large-cap growth zigs, your small-cap or value holdings may zag, enabling you to sustain performance even in bearish times. Of course, these asset classes aren't perfectly negatively correlated so it's not going to be a flawless zig/zag relationship (nothing is unless you're shorting and long in the same position, which would be pretty pointless), but at least it presumably provides protection against the downside while at the same time increasing your expected return. A double win!

As stated above with the Fama French Model, but it doesn't hurt to emphasize this point, since small-caps and value typically carry larger risks, the expected return must be greater to compensate. This is the small-value premium that people seek.

What this means for your portfolio

Personally, I think it makes the most sense for individual investors to simply hold small-cap value and ignore small-blend and large value. I find this simplified approach meets the desired results and is easier to hold and maintain in a tax efficient manner. Some aggressive investors prefer a 50/50 split between total stock and small-value. I personally like approximately a 2:1 total stock to small value ratio. Value, small-cap, and small-cap value funds are typically less tax efficient than a total stock market fund counterpart, so it probably makes sense to hold the small-cap value in retirement accounts. Although examining the tax cost ratio via Morningstar of a fund like VISVX (Vanguard Small-Cap Value Index) shows the difference is negligible (in fact, VISVX seems to be more tax efficient than VTSMX over certain periods) , so holding it in taxable account certainly isn't the worst thing you could do.

Remember the media calling 2000-2010 the "lost decade" as the S&P was virtually unchanged? Well, if you had invested a considerable sum in small-cap value, your portfolio would be in seriously positive territory for that period. Not so lost anymore! From January 14, 2000 to June 10, 2010 (today), Vanguard Total Stock Market is down nearly 17%. It certainly would seem like a waste of investments if that was your return after 10 whole years. VISVX, on the other hand, is up 64% over the same period - an outperformance of 81%! And you thought those timing strategies had good outperformance. This strategy simply calls for setting a slightly different asset allocation and letting it be (which is much more tax efficient) and absolutely obliterated more complicated, tax-inefficient strategies.

Let's take a look at the growth of $10,000 chart of Total Stock Market and Small-Cap Value since June 1998. The blue line is total stock, while the orange line is small value.

(Source: Morningstar Inc.)

In the end, after twelve years your $10,000 invested in VTSMX grew to nearly $12,000, while small-cap value blossomed to nearly $19,500. That's the small-cap premium we're looking for!

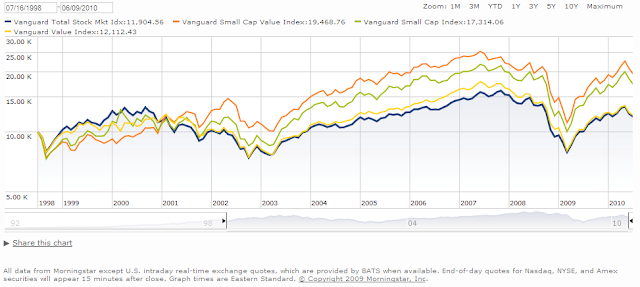

Just as a comparision, here is a chart comparing total stock (blue) with value (yellow), small blend (green), and small-value (orange). As you can see (although this won't always be the case), small-value really provides the best of both worlds in the Fama French model.

(Source: Morningstar Inc.)

The Value Index largely mirrored total stock (although provided some refuge during the growth uprun and demolition from 1998-2003), while small-blend provided more diversification, and small-value gave even a larger return due to its premium.This strategy should be in the arsenal of all indexing individual investors. Small-cap value provides greater expected return and increased diversification with the caveat that one should expect slightly more volatility and risk.

Edit: DIY Investor brought up a good point in the comments that investors with lower risk tolerances (e.g. retirees) might want to think twice before "loading up" on these asset classes based on the downside risk, standard deviation, and volatility measures. I certainly agree and probably should have mentioned this above as there is certainly is increased risk in these asset classes. However, as I responded, I think investors are more than amply compensated for the additional risk. A retiree with a 40/60 equities/bonds portfolio might have something like 20% Total US, 10% Foreign, and 10% US Small Value based on my proposed 2:1 US Total to small value. 10% Small-Value, even with its volatility, is not going to wreak havoc on that portfolio and would marginally increase your risk (while correspondingly increasing your expected return). Looking at the alpha measures of VISVX (quite simply, a risk-adjusted measure of performance; of course, past performance doesn't guarantee future results), VISVX has a 3-year alpha of 6.68 (with a beta of 1.28) and a 1-year alpha of 6.68. That is, VISVX has enjoyed nearly a 7% outperformance (annually) of what CAPM would predict (i.e. after taking risk/beta/volatility into account). VTSMX, for comparison has an alpha of 1.18 (and beta of 1.03, as expected). As stated, this doesn't guarantee anything for the future, but historically the alpha values for small-value are favorable and investors have been more than compensated for the increased risk. But, it is important to stress, that the increased risk is real, so you should take this into account if you plan to dip in this asset class.

Update 6/16/10: Larry Swedroe's recent article on why the Small Growth Index is the "Black Hole of Investing." That's why I avoid it all together.